Retirement Plan Contribution Limits for 2018

Each year the IRS makes cost of living adjustments to many of the limits on benefits from - and contributions to - qualified and non-qualified retirement plans. Here are the new limits for 2018:

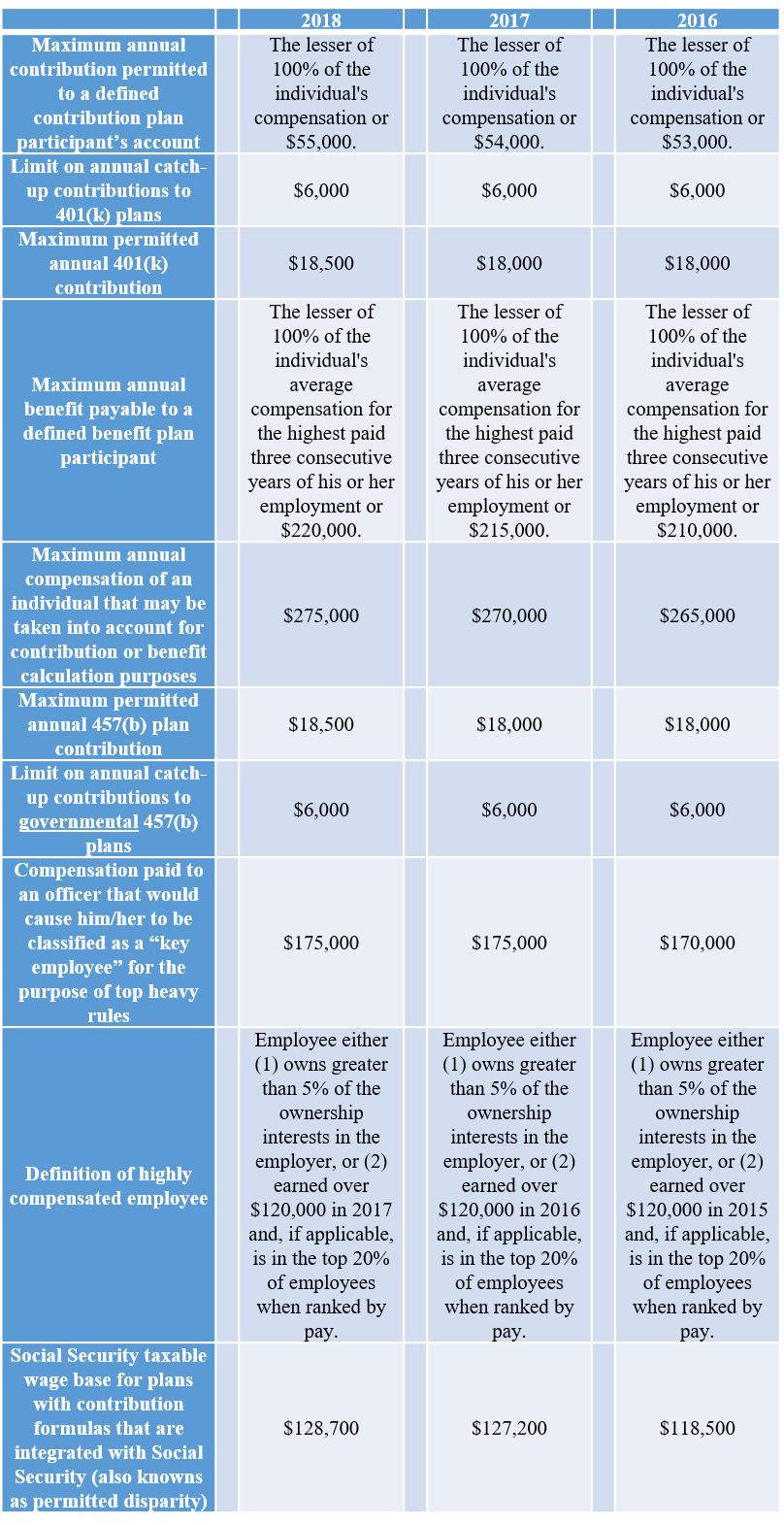

- The maximum annual contribution to an individual’s account in a defined contribution plan (a money-purchase, profit sharing and/or 401(k) plan) cannot exceed the lesser of 100% of the individual’s compensation or $55,000. That amount is $1,000 more than the 2017 limitation and it includes employer contributions, employee 401(k) contributions and forfeitures. If your defined contribution plan has a fiscal year other than the calendar year, this new limit is effective for plan limitation years ending in 2018. An individual who is 50 or older in 2018 and participates in a 401(k) plan can make an additional 401(k) “catch-up” contribution of up to $6,000 over and above the $55,000 amount. This “catch-up” limit is unchanged from the 2017 “catch-up” limit.

- The maximum annual 401(k) contribution an individual can make is $18,500 ($500 more than the 2017 limit). An individual who is 50 or older in 2018 can make an additional “catch-up” 401(k) contribution of up to $6,000 (unchanged from the 2017 limit) over and above the $18,500 limit. These limitations include Roth 401(k) contributions; in other words, total 401(k) contributions are limited to $18,500 (plus the $6,000 catch-up amount if applicable) regardless of how much of the total comes from “pre-tax” 401(k) contributions and how much from Roth 401(k) contributions.

- The maximum annual benefit which may be paid to an individual in a defined benefit plan is the lesser of 100% of the individual’s average compensation for the highest paid three consecutive years of his or her employment, or $220,000, which is $5,000 higher than the 2017 limitation. If your defined benefit plan has a fiscal year other than the calendar year, this limit is effective for plan limitation years ending in 2018.

- The maximum amount of an employee’s annual compensation which may be taken into account for contribution or benefit calculation purposes is $275,000, effective for plan years beginning in 2018. This represents a $5,000 increase from the 2017 limitation. If your plan has a fiscal year other than the calendar year, this limit is effective for plan limitation years beginning in 2018.

- For tax-exempt entities, the maximum amount which an individual may contribute to a 457(b) plan is $18,500 ($500 more than the 2017 limit). The “catch-up” contribution in a government-sponsored 457(b) plan for an individual who is age 50 or older in 2018 is up to $6,000 over above the $18,500 contribution limit. This “catch-up” limit is the same as the 2017 “catch-up” limit.

- Special rules apply to “top heavy” plans. A defined contribution plan is top heavy if the aggregate account balances of key employees exceed 60% of the aggregate account balances of all plan participants. A defined benefit plan is top heavy if the present value of the accrued benefits of key employees exceeds 60% of the present value of the accrued benefits of all plan participants. For 2018, the compensation paid to an officer that would cause him or her to be classified as a “key employee” remains at $175,000.

- A retirement plan may not discriminate in favor of “highly compensated” employees. An employee is a highly compensated employee in 2015 if the employee either (1) owns greater than 5% of the ownership interests in the employer, or (2) earned over $120,000 in 2017 and, if applicable, is in the top 20% of employees when ranked by pay. For purposes of determining who will be a highly compensated employee in 2018, the dollar limitation has not increased.

- The Social Security taxable wage base used in plans whose contribution formulas are integrated with Social Security (this is also referred to as permitted disparity) is increased in 2018 from $127,200 to $128,700.

On a fairly regular basis, employers should review their plan’s design to ensure that the key employees are benefiting from the increased contributions, and that the plan is operating as a valuable recruitment and retention tool. You may want us to review your current retirement plan to make sure it maximizes the potential benefits and is consistent with the overall objectives of the organization. Please feel free to contact us:

Paula A. Calimafde, Esq. - 301.951.9325 - calimafd@paleyrothman.com

Arnold B. Sherman, Esq. - 301.951.9377 - asherman@paleyrothman.com

Jessica B. Summers, Esq. - 301.968.3402 - jsummers@paleyrothman.com

The table below sets forth the limitations for 2018 together with the 2016 and 2017 limitations: